Credit rationing

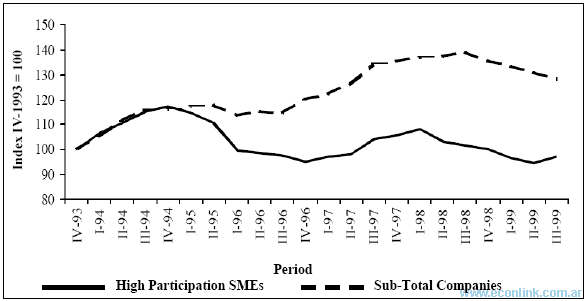

In first place we can check empirical evidence that shows credit rationing effect to the SMEs in the Argentinean financial sector. It’s possible to verify an increasing spread between the amounts lent to SME and the rest of the private sector on the second half of the decade. It is quite evident the coincidence in between the beginning of the concentration process and the increase on the spread; over the same period the total funds lent to the private sector were growing and the amount assigned to SMEs was stagnated and even decreasing, thus we can say that existed an adjustment via volume (see Figure 6).

Figure 6. BANKINING CREDIT EVOLUTION BY SECTOR. ARGENTINA

1993/1998.

Source: Translated from Aramburu (2000).

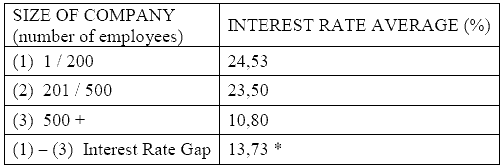

As second empirical evidence we found that the interest rates applied were constantly high during the same period maintaining an average spread of 13,5% higher than the rate applied to larger companies, thus there wasn’t a price adjustment via interest rate (See Table 5 and Figure 7).

Table 5. INTEREST RATES BY SIZE OF COMPANY. ARGENTINA -

AVERAGE 1994/2000

This gap is observed steady along the decade

Source: F.I.E.L. (1996).

Note: The spread was calculated over the average rate applied to SMEs and large companies. In coincidence this is the spread observed along the period between the SMEs average and PRIME rates.

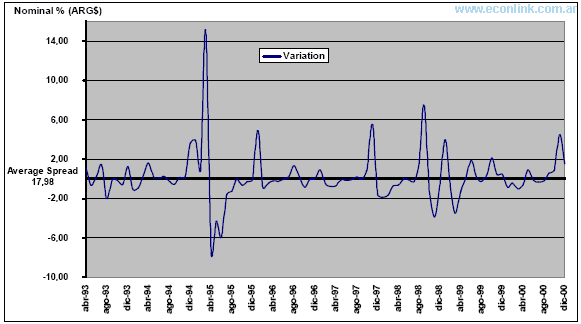

Figure 7. EVOLUTION INTEREST RATE SPREAD. PRIME / OVERDRFAT

CURRENT ACCOUNT. ARGENTINA 1993/2000.

Source: Author. Data from BCRA.

Note: Variation on the spread between the interest rate applied to ‘Prime’ loans and overdraft current account. Prime rate: Is the interest rate that the banks apply to their better subjects of commercial credit and to his greater corporative clients. The banks use the PRIME rate as reference to establish the rates for credit cards, loans to mortgages houses and other types of loans, including loans for small and medium businesses.

Finally taking into account that the economy grew at an average rate of 6% and the participation of the SMEs on the GDP was steady around 30/40% along the same period, we can assume that the decrease in financing was not followed by a decrease in the SME participation in the economy, thus the sector maintained his relative size or even increased it.

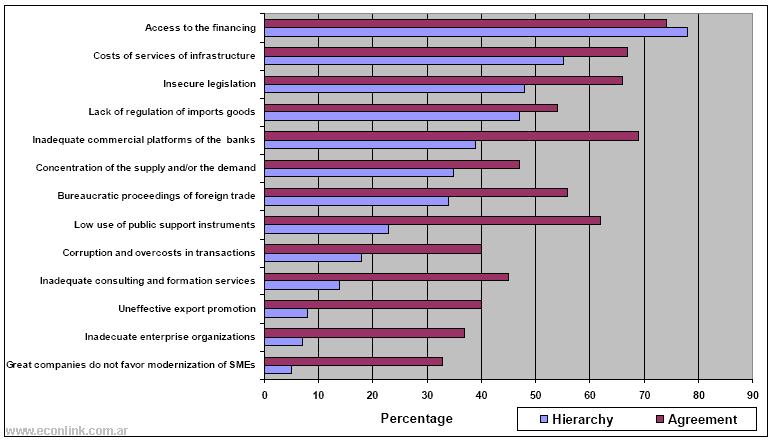

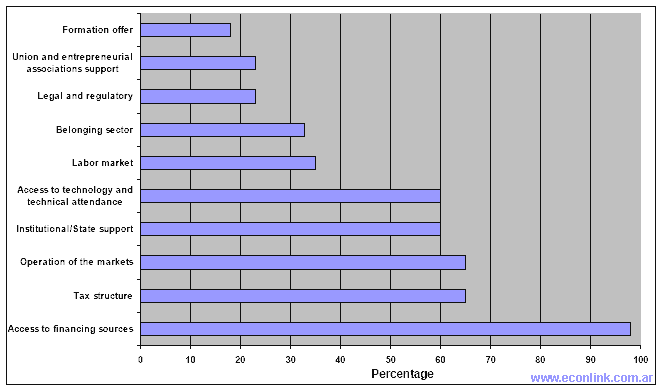

This evidence of credit rationing from the point of view of the financial system (the previous data is collected form banks side) is supported by the results found in the SMEs sector and even more this situation was recognized by the Institutional sector. A study performed at the end of the decade (Yoguel, 1999) in between 57 organizations of different types confirmed that the problems related to credit access were the main factor that prevented the creation and development of businesses in the SMEs sector. As a result 77% of the SMEs adduced that interest rates, terms and collaterals required were the main problem of their business, and most of them had loosed new business opportunities due to the lack of financing. Confirming this priority the 98% of Official and Private Institutions recognized that the access to credit were the first problem of the sector (See Figures 8 and 9).

Figure 8. MAIN DIFFICULTIES MANIFESTED BY SMEs COMPANIES.

ARGENTINA 1999.

Source: Translated from FUNDES-UNGS (1999).

Figure 9. SMEs MAIN DIFFICULTIES MANIFESTED BY THE

INSTITUTIONS. ARGENTINA 1999.

Source: Translated from Yoguel (1999).

Anonimo (01 de Sep de 2008). "Credit rationing". [en linea]

Dirección URL: https://www.econlink.com.ar/information-banking/argentina-credit-rationing (Consultado el 14 de Mayo de 2021)